Credit ScoreNovember 8, 2022Is It Possible To Have A High Credit Score Despite A Rising Credit Balance? Read More

Bad CreditMarch 28, 2017Debt Consolidation Loans for Those With Bad Credit — Frequently Asked Questions Read More

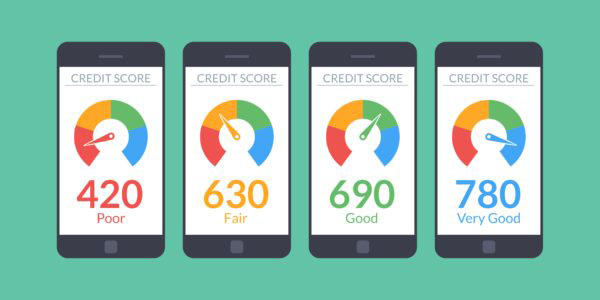

Credit ScoreFebruary 17, 2014Think You Have Good Credit? Know The 8 Credit Score Ranges To Be Sure Read More