Retiree Debt Relief

- Many retirees carry debt into retirement, including credit card, mortgage, and medical debt.

- Common causes of debt include inflation, limited income, rising healthcare costs, and family support.

- Debt in retirement can lead to stress, tough lifestyle changes, and delayed or altered retirement plans.

- Practical steps include budgeting, downsizing, delaying benefits, cutting expenses, and working part-time.

- Seniors may benefit from tailored debt relief solutions, including consolidation, counseling, or settlement.

If you’re nearing or already in retirement and struggling with debt, you’re not alone. Many older adults find that financial challenges don’t disappear after leaving the workforce—in fact, they can become even more difficult to manage on a fixed income.

For decades, older adults were expected to retire with financial security, enjoying the benefits of decades of hard work. However, for many, the reality is far different. Instead of financial freedom, a significant number of retirees are carrying substantial debt into their retirement years, creating stress and uncertainty about their financial future.

From rising living costs to unexpected medical bills, there are many reasons why debt can follow people into retirement. The good news is that there are ways to reduce the burden, regain control of your finances, and make the most of your retirement years.

Free Consultation with a Certified Debt Specialist

Start with a Free No-Obligation Consultation

If you’re nearing or already in retirement and struggling with debt, you’re not alone. Many older adults find that financial challenges don’t disappear after leaving the workforce—in fact, they can become even more difficult to manage on a fixed income.

For decades, older adults were expected to retire with financial security, enjoying the benefits of decades of hard work. However, for many, the reality is far different. Instead of financial freedom, a significant number of retirees are carrying substantial debt into their retirement years, creating stress and uncertainty about their financial future.

From rising living costs to unexpected medical bills, there are many reasons why debt can follow people into retirement. The good news is that there are ways to reduce the burden, regain control of your finances, and make the most of your retirement years.

Start Paying off Your Retirement Debt Today!

The Growing Debt Burden Among Retirees

Data shows that older adults hold an alarming amount of debt, making financial stability in retirement increasingly difficult to achieve:

- As of 2024, Baby Boomers carry a total of $4.5 trillion in debt, according to an Experian consumer debt study.

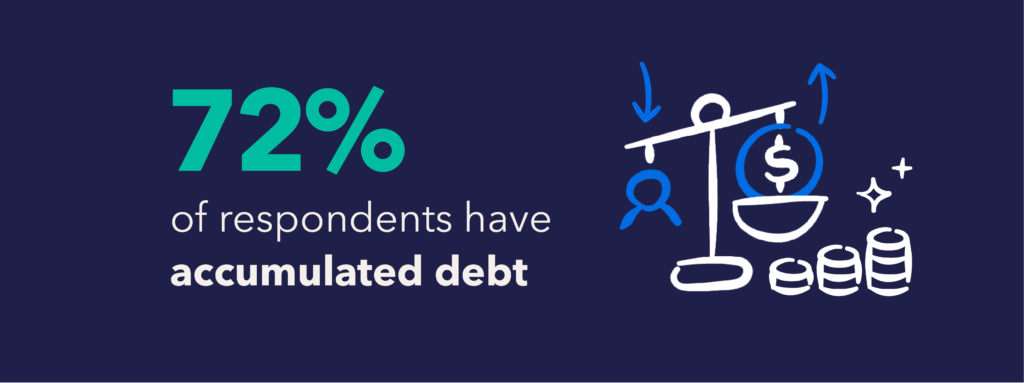

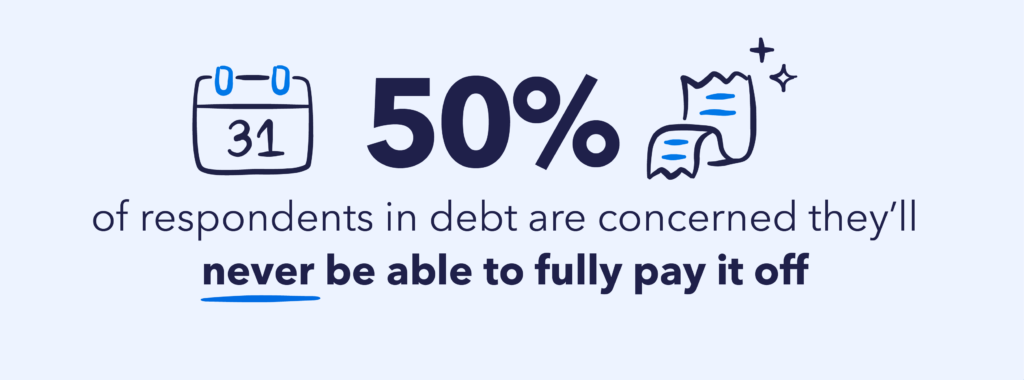

- In a 2025 survey commissioned by National Debt Relief and conducted by Talker Research, 72% of Americans aged 55–78 reported carrying some form of debt, and 50% said they feel overwhelmed and fear they’ll never pay it off.

- A 2019 study conducted by the Center for Retirement Research at Boston College found that one in four households over the age of 65 still has a mortgage. This goes against the traditional expectation of entering retirement debt-free.

- According to Bankrate, 83% of Baby Boomers have at least one credit card. 45% of those who do use credit cards will carry a balance each month.

- Medical debt is another challenge, with nearly 4 million adults aged 65 and older struggling with unpaid medical bills, per the Consumer Financial Protection Bureau.

- Even auto loans remain a factor, with a 2023 Credit Karma study finding that Baby Boomers carry an average of $21,000 to $22,000 in vehicle-related debt.

The Emotional Toll of Debt in Retirement

Beyond the financial strain, debt carries a significant emotional burden for retirees. Many older adults face stress, uncertainty, and fear of outliving their savings, leading to increased anxiety about their ability to afford everyday expenses. The pressure of managing debt on a fixed income can result in difficult choices, such as delaying healthcare, cutting back on necessities, or even postponing retirement altogether.

For those already retired, the challenge of balancing debt with limited income from Social Security, pensions, and savings can create a cycle of worry. Many retirees wonder if they will need to re-enter the workforce or downsize their lifestyle to stay afloat financially.

source: Bankers Life Center for a Secure Retirement

Causes of Retiree Debt

Older adults were once expected to retire with financial freedom, but for many, debt has become a growing concern. Understanding the root causes of this trend can be the first step to finding viable solutions.

Rising Cost of Living and Inflation

The cost of essentials—housing, healthcare, food, and utilities—has increased significantly over time. Many currently retired people did not anticipate these rising costs when they were planning for retirement. Inflation, especially during the last few years, has further strained fixed incomes, forcing some retirees to rely on credit cards or loans to cover basic expenses.

- From 2020 to 2025, the U.S. experienced an average annual inflation rate of 4.18%, leading to a cumulative price increase of 22.74%.

- The Consumer Price Index has risen 21.7% since the pandemic, making everyday essentials significantly more expensive.

- Electricity prices alone increased by 2.8% in 2024, following a 3.3% rise in 2023, putting additional strain on retirees’ budgets.

source: 2025 National Debt Relief survey

Mortgage Debt in Retirement

The burden of mortgage debt has become a growing concern for older adults, many of whom expected to retire with fully paid-off homes. However, a significant portion still carry mortgage payments into their retirement years, adding financial strain. Rising housing costs and economic shifts have contributed to this ongoing debt burden.

- As of the third quarter of 2024, Baby Boomers carried an average mortgage debt of approximately $191,557, making housing debt one of their largest financial obligations.

- A 2024 study found that one in four retirees is still making mortgage payments, significantly impacting their financial security and monthly budgets.

source: 2023 American Community Survey

Credit Card Reliance

Many Baby Boomers increasingly rely on credit cards to manage daily expenses such as groceries, utilities, and medical bills. This dependency has led to a notable accumulation of credit card debt within this demographic.

- As of 2023, Baby Boomers carry an average credit card debt of approximately $6,601. This figure positions them with the second-highest credit card debt among all age groups, following Generation X.

- On average, Baby Boomers possess 3 credit cards per individual, indicating a widespread reliance on credit for financial management.

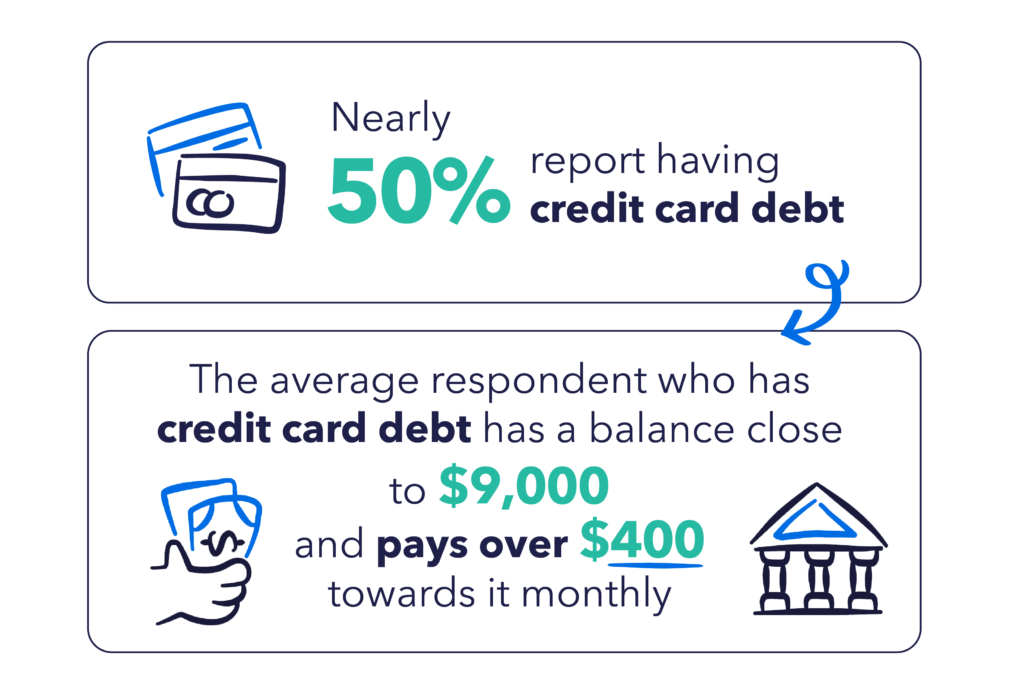

- A 2025 National Debt Relief survey found that 45% of Americans aged 55–78 have credit card debt. Among those, the average balance is nearly $9,000, with monthly payments averaging $418.

Medical Expenses and Healthcare Debt

Even with Medicare, healthcare costs remain a significant financial burden for older adults. Out-of-pocket expenses, prescription costs, and unexpected medical bills have forced many retirees to rely on credit or dip into their savings.

- According to the Consumer Financial Protection Bureau, nearly 4 million adults aged 65 and older struggle with unpaid medical bills.

- A 2023 Fidelity Retiree Health Care Cost Estimate found that the average 65-year-old couple will need approximately $315,000 to cover healthcare expenses throughout retirement.

- In a 2025 National Debt Relief survey, 17% of respondents aged 55–78 reported having medical debt. On average, they owed $9,144 and were paying $222 a month toward it.

- Many retirees find that Medicare does not cover essential expenses like dental, vision, and long-term care, leading to additional out-of-pocket costs and debt.

source: 2024 ValuePenguin study

Supporting Adult Children and Family Members

Many older adults continue to financially support adult children or even grandchildren, often at the expense of their own financial well-being. Economic challenges, student loan debt, and housing affordability issues have led many younger generations to rely on their parents for financial assistance.

- A 2024 Bankrate survey found that 56% of Baby Boomer parents have made financial sacrifices to assist their adult children, covering expenses such as housing, student loans, and daily living costs.

- Those who financially support family members are more likely to carry debt into retirement, as these unplanned expenses can limit their ability to save or pay off existing obligations.

Insufficient Income

Many older adults experience a decrease in income upon retiring, and often, payouts from retirement funds and Social Security aren’t keeping up with today’s cost of living. This financial gap can lead to increased debt as retirees struggle to cover standard living expenses such as housing, food, and healthcare.

- The Transamerica Center for Retirement Studies reported in 2023 that the median retirement savings for Baby Boomers was $289,000, which may be insufficient to cover living expenses.

- According to the Social Security Administration, Social Security benefits represent only 31% of the income of people aged 65 and older.

- The average monthly Supplemental Security Income (SSI) benefit for Americans 65 or older in January 2025 was only $590.16, per a report by the Social Security Administration.

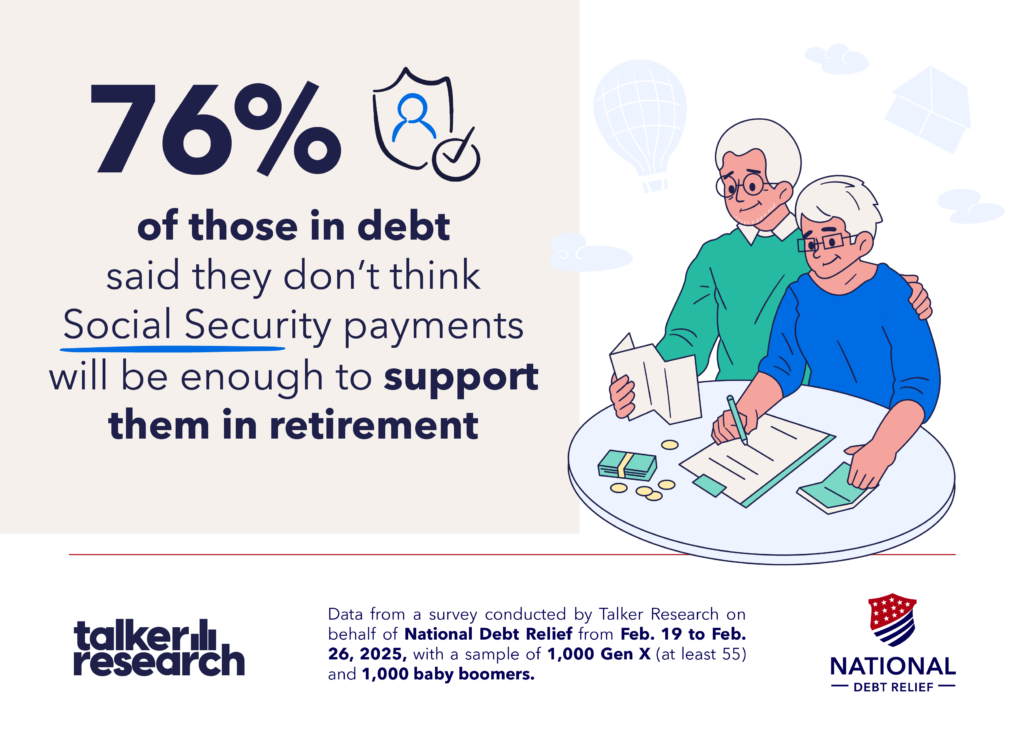

- 76% of respondents in a 2025 National Debt Relief survey said they don’t believe Social Security payments will be enough to support them through retirement.

Increased Life Expectancy

Advancements in healthcare and living conditions have led to a significant increase in life expectancy over the past century. While this is a positive development, it also means that retirees need to plan for longer periods without employment income, increasing the risk of outliving their savings.

- As of 2023, life expectancy at birth in the U.S. increased to 78.4 years, up from 77.5 years in 2022, though still below the pre-pandemic estimate of 78.8 years in 2019.

- A 2024 Clever survey revealed that 40% of retirees are concerned about outliving their retirement savings, highlighting the financial challenges posed by increased life expectancy.

Long-Term Care Costs

The rising costs of long-term care present a significant financial challenge for many older adults, often leading to unexpected debt. Medicare generally doesn’t cover long-term care costs, including stays in nursing homes or assisted living facilities, or costs for home care. Medicare primarily covers medically necessary care, and long-term care is often custodial care. As a result, retirees facing chronic illnesses, mobility issues, or cognitive decline often turn to personal savings, credit, or even debt to afford necessary care.

- The Administration on Aging found that someone turning 65 in 2020 had nearly a 70% chance of requiring long-term care at some point.

- In 2019, the U.S. Department of Health and Human Services released a study showing that individuals who require long-term care services typically need them for an average of 3.2 years. Additionally, more than 20% of those individuals need long-term care for five years or longer.

- The 2021 Cost of Care Survey from the Federal Long Term Care Insurance Program reported that the annual average of facility-based care ranged from $57,912 for space in an assisted living facility all the way up to $114,975 for a private room in a nursing home.

source: 2019 Pan American Health Organization press release

How Debt Impacts Retirement and Financial Security

Debt can turn what should be a relaxing and fulfilling stage of life into a period of stress and financial strain. Instead of using their retirement income for essentials and leisure, many retirees find themselves struggling to keep up with debt payments. This not only affects financial stability but can also take a toll on overall well-being.

Debt Can Force Difficult Lifestyle Changes

When debt becomes unmanageable, some retirees are faced with tough choices. They may end up:

- Returning to Work: Many retirees who planned to enjoy their golden years in leisure find themselves searching for part-time jobs just to cover debt payments.

- Downsizing: Selling a home or moving to a less expensive area might be the only way to free up cash and reduce expenses.

- Cutting Back on Support for Family: Some retirees who once helped their children or grandchildren financially may no longer be able to provide assistance.

These changes can feel discouraging, especially for those who expected a stress-free retirement. But while debt can create financial challenges, it doesn’t have to define the retirement experience.

How to Avoid Retiree Debt

While debt in retirement is increasingly common, there are proactive steps you can take to protect your financial future.

Multiple options exist for older adults, especially those with limited resources, who are facing financial challenges in retirement. Like budgeting strategies at any age, many involve lifestyle changes (including downsized housing) and shopping around for products and services (e.g., health care). Income-based public benefits (if qualified) may be another resource. The less debt people carry into retirement, the more financial flexibility and resilience they will have in later life.

Create a Realistic Retirement Budget

A well-structured budget can help retirees manage expenses and avoid unnecessary debt. Since income often becomes fixed after retirement, it’s important to plan accordingly.

Step 1: List All Income Sources

Your income streams now that you’re retired are likely different than what they were when you were working. Some common sources of retirement income include:

- Social Security Benefits

- Pensions or annuities

- 401(k) or IRA withdrawals

- Savings and investments

Step 2: Categorize and Track Expenses

To create a budget you can actually stick to, you’ll first need to have a clear picture of all your expenses. It can be helpful to separate them into categories.

Fixed Expenses:

- Mortgage or rent

- Property taxes and homeowners’ insurance

- Utilities (electricity, water, internet)

- Insurance (health, life, long-term care)

- Minimum debt payments

Variable Expenses:

- Groceries and dining out

- Transportation (gas, maintenance, public transit)

- Medical costs (prescriptions, co-pays)

- Household maintenance

Discretionary Expenses:

- Travel and vacations

- Entertainment and hobbies

- Charitable donations

- Gifts for family and friends

Step 3: Expect the Unexpected

Even the best-planned budgets can be derailed by emergencies. It’s important to keep enough funds on hand to cover things like sudden medical or dental bills, unexpected home repairs, or family emergencies (such as travel costs for a funeral).

To create an emergency fund, you can:

- Set a savings goal: Aim for three to six months’ worth of essential expenses.

- Open a dedicated account: Use a high-yield savings account for easy access and growth.

- Automate your savings: Set up automatic transfers to your emergency fund.

Step 4: Adjust as Needed

Your financial needs will change over time, which means your budget will need to change along with them. Some key times to reassess your budget are:

- Annually to adjust for inflation and an increased cost of living

- After major life changes such as moving, a health diagnosis, or death of a spouse

- When RMDs begin (age 73 for people born from 1951-1959 and age 75 for those born in 1960 and later) so that you can plan for required IRA/401(k) withdrawals to avoid penalties

Live Within Your Means

One of the best ways to maintain financial stability in retirement is by adjusting your lifestyle to fit your available income. Living within your means ensures you can cover necessary expenses without accumulating debt.

How to Reduce Housing Costs

Housing is one of the largest expense for retirees. Downsizing or making adjustments can significantly lower monthly costs. Here are some strategies to try:

- Move Into a Smaller Home: If you no longer have kids at home, you might not need that four-bedroom house anymore. Selling it and moving into a smaller house or condo can reduce your mortgage payments, property taxes, and maintenance costs.

- Relocate to a Lower-Cost Area: Consider moving to a state with lower living costs, reduced property taxes, and/or no income tax. If you’re no longer tied to a specific location for work, now can also be a great opportunity to put down roots somewhere you’ve always dreamed of living.

- Look Into Senior Housing Communities: In addition to benefits like social activities and easier access to healthcare, many offer lower maintenance and utility costs than you might have living alone.

How to Reduce Everyday Expenses

Cutting unnecessary spending can make retirement savings last longer. Here are a few ideas:

- Limit Discretionary Spending: Be honest with yourself about the cost vs. benefit of things like dining out or subscription services. Would you be just as happy if you had friends over for dinner rather than meeting them at restaurants? Are you using both your Hulu and Netflix accounts, or can you get rid of one of them?

- Use Senior Discounts: Many retailers, restaurants, and service providers offer discounts for older adults. If you don’t know if one is offered, there’s no harm in asking.

- Take Public Transportation: If the area where you live has a good public transport system, you could save money on insurance, gas, and maintenance by selling your car and switching to the bus or train instead.

How to Reduce Healthcare Costs

Medical expenses can be a major burden in retirement, but there are ways to manage costs:

- Review Medicare Plans Annually: Make sure you’re on the best plan for your needs. The gov Plan Finder is a good resource to compare options, as is a local State Health Insurance Assistance Program (SHIP) office

- Use Generic Prescriptions: There’s no need to pay for brand-name drugs when you can get the same thing at a fraction of the cost. You can also use GoodRx or SingleCare to compare prescription drug prices at different pharmacies and find discount coupons.

- Take Advantage of Preventive Care: Don’t miss your annual wellness visits! Catching health issues early can reduce long-term medical costs.

Minimize Credit Card Use

Credit card debt can quickly accumulate due to high interest rates. If you rely too much on credit cards, it can be tempting to carry a balance from month to month. To help avoid credit card debt, you can:

- Use Cash or Debit Cards for Everyday Purchases: Some people use the envelope budget method, which is when you put a set amount of cash into envelopes labeled with different spending categories. If you prefer plastic over cash, you could consider switching to a debit card instead.

- Pay Off Your Balances in Full Each Month: Setting up automatic payments will make sure you don’t get hit with high interest simply because you forgot to pay your bill. In cases where you can’t afford to make the full payment, anything above the minimum will help.

- Be Careful With Rewards Cards: There are a lot of credit cards that offer points and rewards to entice you to spend more, but the value of the points may not be enough to outweigh the high interest. Make sure you’re thinking critically about how you use rewards cards (and if you do use them, don’t forget to redeem your points before they expire).

Consider Delaying Social Security for Higher Benefits

Delaying Social Security benefits could increase your long-term retirement income. For retirees who can afford to wait, each year of delay between age 62 and 70 can significantly increase monthly benefit payments. But whether it’s the right move depends on your unique financial situation, health, and retirement goals.

Why Delaying Might Be Worth It

For every year you delay past your full retirement age (which is currently increasing by two months between age 66 and 67), your benefit increases by roughly 8% per year up until age 70.

Here’s how the timing of your claim affects your monthly benefit:

- Claim Early (as early as 62): You’ll receive a reduced benefit, as low as 70–75% of your full amount, depending on how many months before full retirement age you claim.

- Claim at Full Retirement Age (66 or 67, depending on your birth year): You’ll receive 100% of your full benefit—this is your baseline monthly payment.

- Delay Beyond Full Retirement Age (up to age 70):

- If your full retirement age is 66 and you wait until 70, you could receive up to 132% of your benefit.

- If your full retirement age is 67 and you wait until 70, your benefit maxes out at 124%.

How to Decide if Delaying Is Right for You

Delaying Social Security benefits isn’t right for everyone. Ask yourself the following:

- Do you have other sources of income that you can rely on in the meantime?

- If you have enough personal savings, pension payments, retirement account withdrawals, or cash infusions from part-time work, you may not need to collect Social Security benefits quite so soon.

- What is your current health and life expectancy?

- If you’re in poor health or have a shorter life expectancy, claiming earlier might make sense so you can access benefits while you’re able to enjoy them. If you expect to live into your 80s or 90s, delaying benefits pays off over time, especially if you reach your late 70s.

- Are you the higher earner in your household?

- Delaying benefits can increase survivor benefits for a lower-earning spouse if you pass away first, so it can be a strategic move for couples.

source: Social Security Administration Benefits Planner

Add New Income Streams

For retirees who need extra income, part-time work or passive income sources can help cover expenses without dipping into savings.

Part-Time Work

Taking on a part-time job can give you more wiggle room in your budget. Below are some ideas to consider.

Flexible and Low-Stress Jobs:

- Seasonal retail work

- Pet sitting or dog walking

- Event staffing

Jobs That Leverage Your Experience:

- Consulting in your former field

- Online tutoring, teaching, or coaching

- Freelancing

Work-From-Home Opportunities:

- Remote customer service or tech support jobs

- Data entry or transcription work

- Virtual assistant roles

Passive Income

Passive income streams take more time to set up, but once they’re in place, you can enjoy ongoing earnings with minimal day-to-day effort. You might consider:

- Renting out a room in your home

- Listing your vacation property on a platform like Airbnb or Vrbo

- Investing in dividend-paying stocks or a real estate investment trust (REIT)

“The first phone call to National Debt Relief was the hardest to make, but I was glad I did it. It’s one of the easiest things I’ve done”

Commonly Asked Questions

What is the average debt at retirement?

The amount of debt someone carries into retirement varies based on income, lifestyle, and location. However, according to MarketWatch, adults aged 65 to 74 had an average debt of $134,950 in 2022, while those 75 and older carried an average of $94,620. This includes mortgage, credit card, auto loan, and personal loan debt. While some retirees are debt-free, many carry balances that can impact their financial security.

What is the average debt of a Baby Boomer?

According to Experian’s 2024 Consumer Credit Review, the average total debt balance for Baby Boomers was $96,984 as of the third quarter of 2024.

This figure encompasses various debt types, including mortgages, credit cards, auto loans, and personal loans. Notably, Baby Boomers’ average debt is slightly lower than the national average of $105,056 for all consumers. This trend reflects a modest increase in debt levels compared to previous years, influenced by factors such as rising living costs and healthcare expenses.

At what age are most people debt-free?

There is no single age when most Americans become debt-free, but studies provide insight into when people tend to pay off their financial obligations. According to the 2024 Northwestern Mutual Planning & Progress Study, 46% of Baby Boomers (ages 60+) report having no personal debt, meaning that more than half still carry some form of debt in retirement.

In past surveys, Americans have expressed a desire to be debt-free in their early 60s. The 2018 Northwestern Mutual Planning & Progress Study reported that people ideally want to pay off all their debts by age 61. However, there is a gap between expectations and reality, as many still hold some form of debt into their later years.

Should you empty retirement accounts to pay off debt?

Withdrawing money from retirement accounts to pay off debt can seem like a practical solution, but it carries potential financial consequences. Retirement funds are designed to support you in later years, and using them too soon may leave you short on income when you need it most.

One of the biggest concerns is tax penalties and income taxes. If you withdraw from a 401(k) or traditional IRA before age 59½, you may face a 10% early withdrawal penalty, plus regular income taxes on the amount taken out.

Beyond taxes, withdrawing from retirement accounts reduces future financial security. The money in these accounts grows through compound interest, and taking out a lump sum could mean missing out on significant long-term earnings. For example, withdrawing $50,000 today could mean losing hundreds of thousands of dollars in potential growth over the next 20–30 years.

In some cases, it may make sense to use retirement savings if the debt has very high interest rates (such as credit card balances above 20%). However, this decision should be made carefully, ideally with the guidance of a financial professional who can help assess the risks and alternatives.

Can you use Social Security benefits to pay off debt?

Yes, Social Security benefits can be used to pay off debt, just like any other source of income. Since these payments are deposited directly into recipients’ bank accounts, they can go toward credit card bills, loans, mortgages, or other expenses. However, because Social Security benefits are often limited, using them to pay off debt may reduce the funds available for necessities like housing, food, and healthcare.

Can creditors take your retirement income?

In most cases, Social Security benefits are protected from garnishment by private creditors. That means if you owe money on a credit card, personal loan, or medical bill, your Social Security income generally cannot be seized to repay those debts. This protection is guaranteed under Section 207 of the Social Security Act, which prohibits the assignment or garnishment of Social Security benefits by most creditors.

However, there are important exceptions. The federal government can legally garnish Social Security benefits to collect on certain debts, including:

- Federal income taxes (via the IRS’s Federal Payment Levy Program)

- Defaulted federal student loans

- Court-ordered child support or alimony

In these cases, up to 15% of your monthly Social Security benefit may be withheld to repay what you owe. For example, if you’ve defaulted on a federal student loan, the government can deduct a portion of your benefits until the debt is resolved.

It’s also important to distinguish between retirement income held in an account and income already withdrawn. While Social Security payments have built-in protections, retirement account withdrawals—like those from 401(k)s or IRAs—are typically not protected once the money enters your bank account. Once commingled with other funds, those assets may be accessible to creditors depending on your state’s laws and whether legal action (like a judgment) has been taken against you.

If you’re concerned about protecting your retirement income from creditors, it may be helpful to consult with a legal or financial professional who understands the rules in your state.

How can you get out of debt when you are retired?

Getting out of debt in retirement often involves a combination of strategies, such as creating a realistic budget, cutting back on expenses, and exploring part-time work or new income streams. Some individuals also consider debt relief options, like consolidation or settlement programs, to reduce what they owe or simplify repayment.

What is the best debt relief for seniors?

The “best” debt relief option depends on your personal financial situation. Some retirees benefit from debt consolidation loans with lower interest rates, while others find debt settlement or credit counseling more effective. It can be helpful to speak with a professional who can walk you through your options and tailor a plan to your unique needs.

“National Debt Relief put together a plan that I could follow and afford. If I just kept making minimum payments it would’ve taken 40 years to pay off.”

All You Need To Know

We’ve put all of our essential resources in one spot. Everything from debt resolution to taking control of your financial future . Need to talk? Our experts are here to help. Call us anytime for a free no-obligation consultation.

Do you have debt from a fixed income?

- Receive A Free Savings Estimate Today

- See How Quickly You Can Be Debt Free

- No Fees Until Your Accounts Are Settled

Essential Reading

The latest debt relief news, tips, and resources from our team.

We have helped over 1.2 million people toward a brighter future.

Now I wake up knowing that I am paying off my debt, it’s like a weight lifted off my chest and I can breathe a bit more.

“The anxiety is gone, I am credit card debt-free. And that right there, I never thought I would be able to say those words, and it just feels so good.”

Michelle saved 23% on her debt

Now I’m able to go on vacation for the first time in a long time- I was able to go and relax. I couldn’t do that before.