Types Of Debt Consolidation Loans

- Debt relief reduces your balance through negotiation, while debt consolidation combines multiple debts into one loan.

- National Debt Relief negotiates with creditors to lower debt, with fees only charged after a successful settlement.

- Debt relief may impact credit scores but often helps clients save more compared to making minimum payments.

- Ideal for individuals with high unsecured debt or financial hardship, often saving about 30-50% on debt.

- Offers resources, specific debt relief options, and a free consultation with debt specialists.

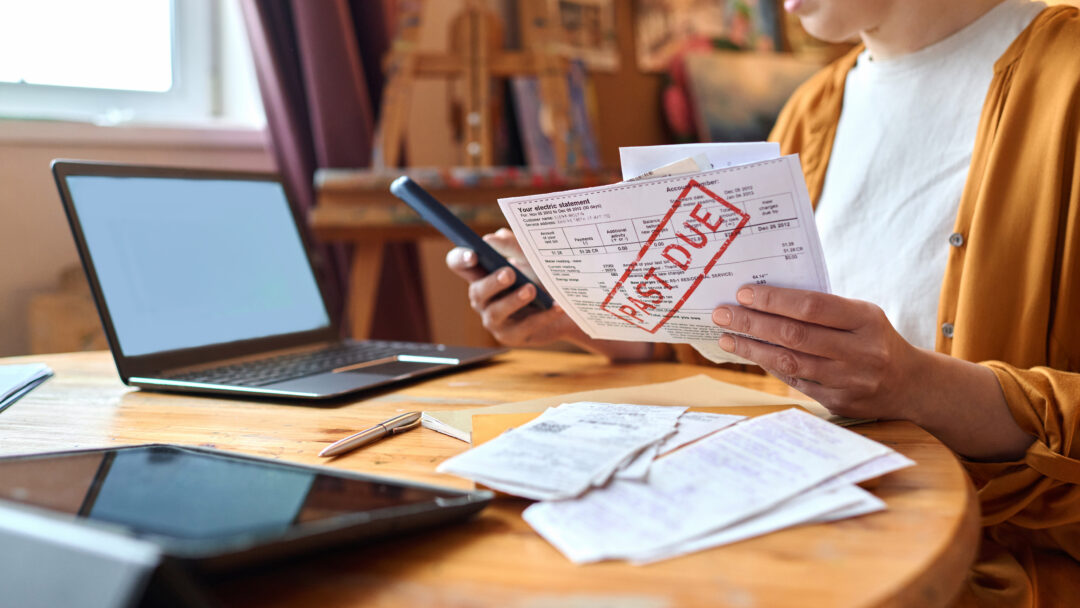

Debt consolidation comes in many forms, with distinct advantages for each. You borrow what you need to pay off your debts and then make a single monthly payment to the lender of the new loan. If you are struggling to keep up with your payments, looking for a way to resolve debt that is less than 50% of your income faster, debt consolidation might be the solution.

Free Consultation with a Certified Debt Specialist

Start with a Free No-Obligation Consultation

Debt consolidation comes in many forms, with distinct advantages for each. You borrow what you need to pay off your debts and then make a single monthly payment to the lender of the new loan. If you are struggling to keep up with your payments, looking for a way to resolve debt that is less than 50% of your income faster, debt consolidation might be the solution.

Start Paying off Your Credit Card Debt Today!

All You Need To Know

We’ve put all of our essential resources in one spot. Everything from debt resolution to taking control of your financial future . Need to talk? Our experts are here to help. Call us anytime for a free no-obligation consultation.

Do You Qualify For Debt Consolidation?

- Discover How Much You Could Save

- See How Quickly You Can Take Back Your Life

- Never Pay A Fee Until An Account Is Settled

Essential Reading

The latest debt relief news, tips, and resources from our team.

We have helped over 1.2 million people toward a brighter future.

Now I wake up knowing that I am paying off my debt, it’s like a weight lifted off my chest and I can breathe a bit more.

“The anxiety is gone, I am credit card debt-free. And that right there, I never thought I would be able to say those words, and it just feels so good.”

Michelle saved 23% on her debt

Now I’m able to go on vacation for the first time in a long time- I was able to go and relax. I couldn’t do that before.