When you log into your loan servicer’s portal, you’ll see a lot of numbers and financial jargon. “Loan principal” is one of many confusing terms you’ll see in your account. But what does “principal” mean in finance, anyway?

In this article, we’ll break down what principal is in a loan, how it’s different from interest, and why paying down principal on a loan is so important.

What Is the “Principal” of a Loan?

The principal of a loan is the original amount you borrow before interest or fees are added. For example, if you take out a $10,000 loan, the principal is $10,000.

The thing to remember about loans is that you aren’t just paying back that $10,000 you borrowed; you’re also paying interest on it. It’s the cost of borrowing the money and how banks make a profit when lending you money.

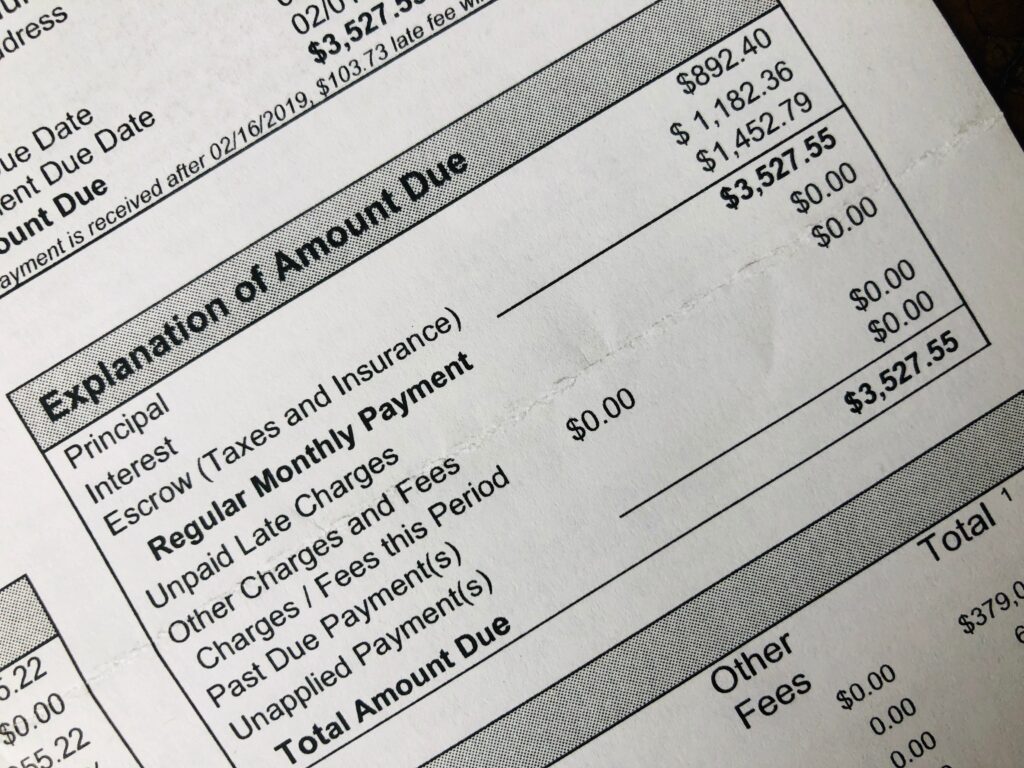

Understanding Your Statement

Loan statements can feel overwhelming at first, especially when you’re juggling bills and trying to stay on top of everything. Here are the most important terms to know.

- Principal: This shows how much of your payment went toward the loan’s principal.

- Interest: Interest is the lender’s fee for lending you money. Your statement will show how much interest you paid during that billing cycle.

- Total payment: This is the full amount you paid for the month, including principal, interest, and any other small fees.

- Remaining balance: This is the total amount you still owe after your monthly payment.

Principal vs Interest: What’s the Difference?

When you make a loan payment, you’re typically paying both principal and interest. Interest is calculated based on your remaining loan balance, so the amount you owe in interest changes over time.

Early in the loan, a larger share of your payment goes toward interest, while a smaller portion reduces your principal. For example, out of a $250 payment, $180 might go to interest and $70 to principal.

As your balance decreases, more of each payment goes toward principal. Later on, that same $250 payment might include $120 in interest and $130 toward principal.

This shift—combined with your interest rate and loan term—is why paying down debt can feel slow at first but accelerates over time.

Take Control of Your Loan by Understanding the Basics

Understanding your loan principal gives you a clearer picture of how your debt works and how to pay it off more efficiently. While interest is the cost of borrowing, it’s the principal that actually determines how much you owe. The faster you reduce it, the less interest you’ll pay over time.

By knowing how your payments are split and how your balance changes, you can make more informed decisions, whether that’s paying extra toward the principal, refinancing, or simply staying consistent with your payments. Small actions can make a meaningful difference, especially over the life of a loan.